Will Legacy Laws Ever Catch Up With Crypto-assets?

Introduction

Pursuant to historical terms and digital years both, it has always been the case that technological innovation goes before the law, and or regulation. This, however, is no different when it comes to crypto-asset emergence and resulting fast and quick-paced revolution, adoption, and implementation by mainstream real economic sector big players across the planet. Though regulators across the world struggle and speed up crypto-regulatory efforts, adoption and mainstreaming processes are on the constant upgrowth direction.The clichéd datapoint is made that while crypto-asset products and services are to an extent, caught by extant mainstream laws and regulations, the Internet commerce blockchain base layer protocol, which is the layer 1 protocol atop with the crypto-asset innovation sits, is totally outside a nation-state regulatory and supervisory reach. This further explains the near impossible sovereign nation-state regulatory matrix quandary, and international standard-setter attempts to reach Decentralised Finance(DeFi) econosphere to rein in, control innovation and regulate for monetary policy integrity, monetary and financial stability, investor protection, investor confidence, data protection policy considerations, KYC/AML-CFT purposes etc.

Private Crypto-assets and Public Crypto-assets

Crypto-assets are peer-to-peer cryptographic infrastructure-based token assets, which could manifest as

iii. cryptosecurities,

vi. cryptoderivatives,

or could be a property piece represented with cryptographic derivative roots. These are any property pieces tokenised and programmed on a blockchain backend technology, or any such cryptographic distributed ledger technology implementing alphanumeric character transaction hash sequence 272ba4844632db8e1e0898a36627bb93f4f909536371f2c10dad8cb4de886c4e. Strategic to a digital or virtual asset (crypto-asset properly so-called), encryption technique is used to generate and regulate crypto-asset units and verify their transactional activities, without any agency whatsoever from a central banking entity. Cryptoassets are a decentralised monetary tool both in nature and character, and offer in a digital form, unique advantages of central banknotes. Some of these are integrity, liquidity and settlement finality.

Source URL link: https://marketbusinessnews.com/financial-glossary/central-bank/

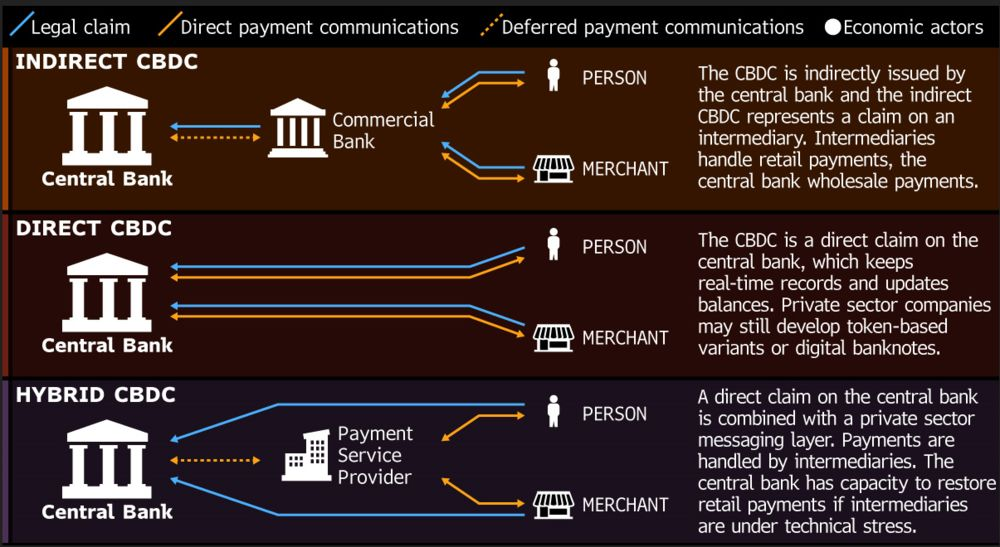

Public Crypto-asset (CBDC) Regulation Implementation Types

Public crypto-assets are cross-border, cross-world transnational in nature, and antithetical to private sector global stablecoin crypto-assets. Sovereigns would have to put heads together to regulate private crypto-assets through taxation, KYC/AML-CFT due diligence conditio sine qua non, set rules, registration requirements, oversight function performance, setting standards and insist on best practices, taskforce efforts etc. measures, while they introduce own sovereign crypto-assets as some Central Bank Digital Currencies(CBDCs) projects are either airdropping, piloting, PoC stage, in research or nearing implementation mainnet. Legislators and regulators would have to make new legal tender laws, and set new rules, policies, regulatory standards etc.

Source URL link: https://www.bloomberg.com/news/articles/2021-03-22/here-s-how-a-central-bank-digital-currency-could-work-chart

CBDC Glocal Adoption Chart Curve

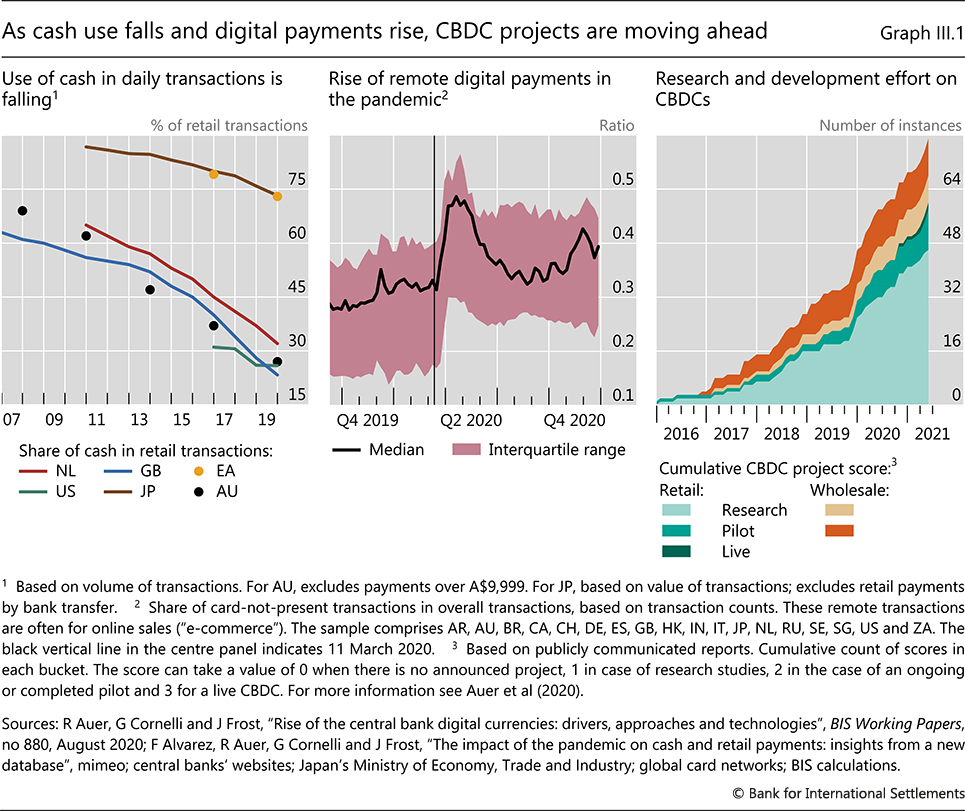

Though CBDCs are not necessarily crypto-assets, the pre-launched/launched CBDC projects so far are crypto-assets i.e. fiat cryptocurrencies China DCEP, Bahamas Sand dollar, e-Naira (CBN CBDC project pilot on Hyperledger to test launch October, 2021) etc. The beneficial CBDC adoption on a global scale is on a monumental high rise speed, as cash use falls and digital payments take off glocally, clearing the way for CBDCs. Cash use in daily transactions fall, as the Covid-19 pandemic raises remote digital payment volume, and CBDC R&D keeps on the northward growth direction.

Source URL link: https://www.bis.org/publ/arpdf/ar2021e3.htm

Major Public Permissionless Open Source Blockchain Networks:

- Bitcoin

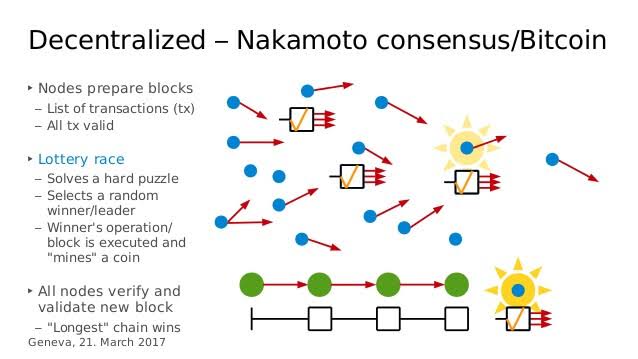

A quick Nakamoto Consensus Bitcoin network environment brief overview reveals that the bitcoin crypto-asset network is resilient because of, among other factors, the shared, decentralised consensus network rules, which are embedded in the network transaction blocks. The Nakamoto Consensus rules set verifies the blockchain authenticity with a Proof of Work (PoW) algorithm atop a Byzantine Fault Tolerance (NFT) peer-to-peer electronic cash payment system network.

- Ethereum

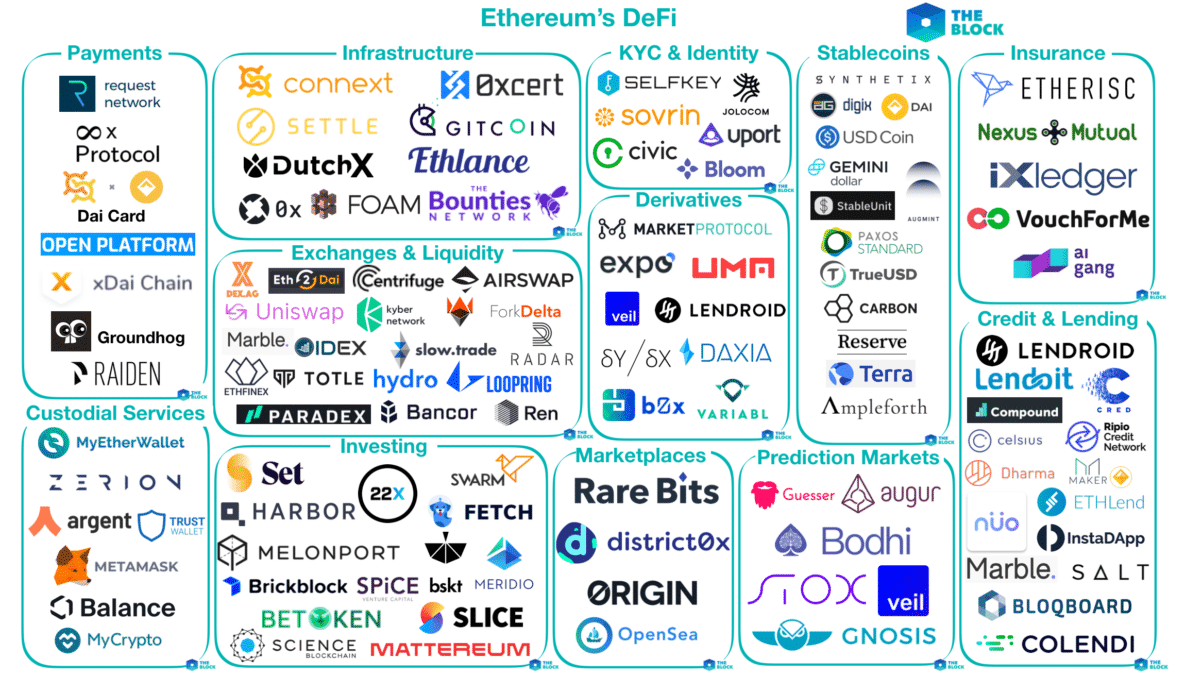

Ethereum DeFi project ecosystem overview:

Though the Ethereum platform is not the only decentralised finance application platform, it is the most comprehensive DeFi platform. There is an ocean of crypto-asset products and related services being built on the Turing-complete EVM through Web3.0 smart contract decentralised applications, i.e. payments, CEX/DEX/HEX infrastructure, KYC & identity, smart contract DeFi, stablecoins, insurance, exchange & liquidity pools, derivatives, credit & lending, custodial services, investing, NFTs, AMM, marketplaces, prediction markets etc.

Source URL link: https://www.bloomberg.com/news/articles/2021-03-22/here-s-how-a-central-bank-digital-currency-could-work-chart

Other blockchain/distributed ledger technology platforms:

Source URL link:https://www.leewayhertz.com/blockchain-platforms-for-top-blockchain-companies/

Toward Crypto-assets Proper Regulation Road

Sovereign nation-states before regulate or make laws applicable to crypto-assets, must acquire first the following:

i. Crypto-asset appreciation and knowledge efficiency gain. This can be done through education, awareness, training programmes, and other information dissemination and sensitisation means. At the moment, regulators and incumbents across the globe are hard-pressed to follow this approach, though a few have launched financial technology hubs across a number of jurisdictions, emphasis is seldom placed on the importance of blockchain cryptocurrency financial technology learning and education.

ii. Collaboration and cooperation. Regulators must collaborate and cooperate with stakeholders in the crypto-community, to be able to effectively supervise affairs, attain and maintain transparency, and hold accountable the blockchain developers, founders, platforms, virtually unregistered virtual organisations, users, consumers, enthusiasts, smart contract engineers and various interests et al., while fighting against cybercriminals and cybercrimes such as hacker password thefts, exit scams, fraudsters who induce reversible transactions et al. From all indications, collaboration and cooperation are important to foster regulation and orderliness in the crypto-asset economic space:

“Unfortunately, these new adopters will encounter a gamut of crimes for which they are ill-prepared: hackers stealing passwords, fraudsters inducing irreversible transactions and exit scams, to name a few. If these same crimes were committed against customers in the banking and brokerage sectors, law enforcement would be piling up arrests and private attorneys would be filing class actions. But the response thus far has been tepid despite a deluge of complaints”.

Conclusion

Though crypto-asset transaction academic data acquisition, understanding and knowledge gain are enlightened, constructive approaches toward proper crypto-regulation, the jury is still out on whether legacy laws will ever be able to catch up with the distributed ledger-based crypto-asset digital transformation revolution. Some of the recent examples nationally and internationally of bespoke crypto-asset statute law jurisdictional attempt to catch up through regulation by taxation, but inadvertently goes way beyond regulating crypto-asset products and servicesis the now passed United States Congress USD1.2 trillion Infrastructure Bill. The Bill generated heated arguments and controversies because it touches upon blockchain consensus layer issues like Proof of Work(PoW) and Proof of Stake(PoS), designating blockchain developers, smart contract engineers, wallet makers etc. as “brokers” for taxation purposes, and the FATF “Travel Rule” crypto application policy is another instance, where the international standard-setting organisation puts out its Recommendation 15 requesting that Crypto-Asset Service Providers(CASPs)/Virtual Asset Service Providers(VASPs) comply, and even extends to embrace DeFi platforms and DEXs as VASPs within the term and definition. Though these are major regulatory attempts and standard-setting efforts, they have not achieved much, or even at the extreme, they have achieved next to nothing, as DeFi and crypto-assets continue to hold sway in the wilds and the “Wild Wild West” anarchy and chaos continue.

Disclaimer

This is for informational purposes only, and not legal, or financial advice, or any advice whatsoever.

Boulevard A. Aladetoyinbo, Esq.

Blockchain & crypto legal advisor, strategy consultant, researcher and trainer.

Lex Futurus (Africa region)

Contact: boulevard@lexfuturus.io